Cash Flow Basics: What Every Small Business Owner Needs to Know

“I have great sales—so why is there no money in the bank?”

If you’ve ever asked yourself that question, you’re not alone. For many business owners, cash flow feels like a mystery. You work hard, invoices go out, customers pay (eventually), but somehow it’s always a scramble to cover payroll or unexpected bills.

Here’s the hard truth: It’s possible to run a profitable business and still go broke—if you don’t manage your cash flow.

The good news? Cash flow doesn’t have to be complicated. In this guide, we’ll break it down into plain language so you can:

✅ Understand what cash flow really means

✅ Avoid common mistakes that drain your cash

✅ Take simple steps to strengthen your cash flow today

Whether you’re just starting out or running an established business, mastering cash flow is one of the smartest things you can do.

What Is Cash Flow (and Why Should You Care)?

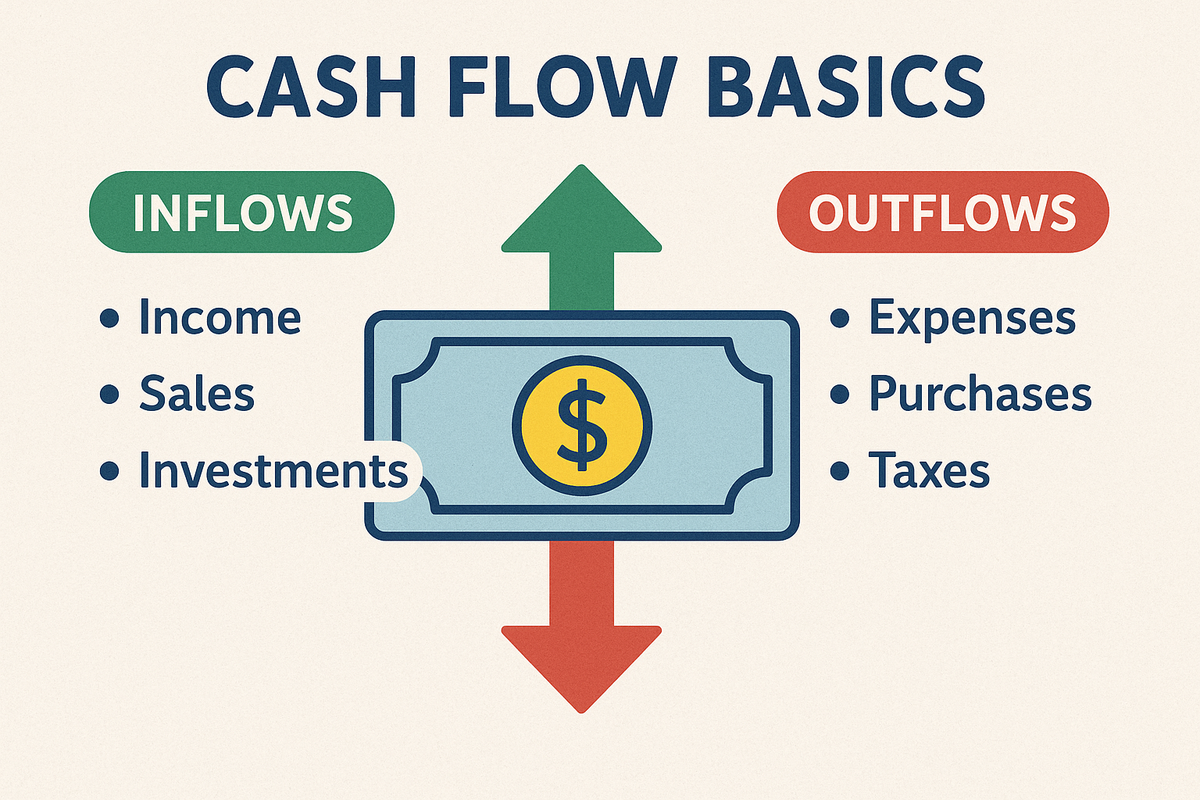

At its simplest, cash flow is the movement of money into and out of your business over a period of time.

Think of it like a bathtub:

- The faucet is cash flowing in—customer payments, loans, investments.

- The drain is cash flowing out—expenses like rent, utilities, payroll, and taxes.

If more water is flowing in than draining out, your tub fills up (positive cash flow). If more water is draining out than coming in, the tub empties (negative cash flow).

Here’s why that matters:

👉 Positive cash flow means you have enough cash on hand to pay your bills, invest in growth, and handle surprises.

👉 Negative cash flow means you’re spending more than you’re earning. Without corrective action, this can lead to missed payments, penalties, and even business closure.

Profit vs. Cash Flow: What’s the Difference?

Many business owners think, “I’m profitable, so I must be okay.” But here’s the catch:

📝 Profit (from your income statement) shows how much you earned after expenses—on paper.

💵 Cash flow (from your cash flow statement) shows how much cash is actually in your bank account.

For example:

- You make a big sale and send an invoice for $50,000.

- It counts as revenue immediately—but if the client takes 90 days to pay, that cash isn’t available to you right now.

- Meanwhile, you still have to pay employees, rent, and suppliers.

That’s why profitable companies sometimes run into cash flow crises.

Why Cash Flow Is the Lifeblood of Your Business

You’ve heard it before: “Cash is king.” But let’s make it practical. Healthy cash flow allows you to:

✅ Keep the lights on – Pay employees, vendors, and taxes on time.

✅ Seize opportunities – Buy inventory at a discount or invest in marketing when the time is right.

✅ Weather storms – Cover unexpected expenses without resorting to expensive loans or credit cards.

📊 A U.S. Bank study found 82% of small business failures are due to poor cash flow management. That’s more than bad products, competition, or economic downturns combined.

Common Cash Flow Mistakes (and How to Avoid Them)

Here are five pitfalls small business owners face:

1. Confusing Profit With Cash

- The trap: Assuming profit = cash on hand.

- The fix: Regularly review your cash flow statement—not just your P&L.

2. Poor Invoicing Practices

- Sending invoices late or not following up results in delayed payments.

- Pro tip: Automate invoicing and send gentle reminders as due dates approach.

3. Overextending Credit

- Relying too much on credit cards or lines of credit can lead to high-interest costs.

- Pro tip: Use credit strategically and only as a short-term buffer.

4. Over-investing in Inventory

- Stocking too much ties up cash you could use elsewhere.

- Pro tip: Monitor inventory turnover and adopt a just-in-time strategy where possible.

5. No Cash Flow Forecasting

- Without a plan, it’s impossible to anticipate shortfalls.

- Pro tip: Create a 12-month cash flow forecast—even a simple spreadsheet will do.

How to Take Control of Your Cash Flow

Here are seven actionable steps to strengthen your cash flow management:

1. Monitor Cash Flow Weekly

Don’t wait until month-end. Check your cash position weekly to stay proactive.

2. Tighten Up Receivables

- Send invoices promptly.

- Offer early payment discounts (e.g., 2% off if paid in 10 days).

- Charge late fees to encourage timely payments.

3. Stretch Payables Without Damaging Relationships

Negotiate longer payment terms with vendors (e.g., 45 days instead of 30) to keep cash in your account longer.

4. Cut Unnecessary Expenses

Audit your expenses. Are there subscriptions or services you no longer use? Trim the fat without hurting operations.

5. Build a Cash Reserve

Aim for at least 3–6 months of operating expenses in an emergency fund. Start small—even saving 1% of revenue is progress.

6. Plan for Seasonality

If your business has busy and slow periods, plan accordingly. Set aside cash during peak times to cover off-seasons.

7. Consider Financing Options (Strategically)

A line of credit can provide a safety net for temporary gaps—but avoid relying on it long term.

Quick Cash Flow Health Check

Ask yourself these four questions:

✅ Do I know my cash balance right now?

✅ Are most customers paying on time?

✅ Could I cover an unexpected $10,000 expense today?

✅ Do I review cash flow at least monthly?

If you said “no” to any of these, take it as a cue to revisit your cash flow strategy.

Key Takeaway

Cash flow isn’t just an accounting term—it’s the fuel that keeps your business running. By understanding how money moves in and out and taking a few proactive steps, you’ll stay in control, reduce stress, and set your business up for long-term success.

💡 Ready to take charge? Download our free Cash Flow Health Checklist to get started!